CBIC has issued clarifications regarding exercise of option to pay tax @3% based on Notification No. 2/2019 Central Tax Rate dt. 7 March 2019, by taxpayers under composition, etc., in respect of first supplies of goods/ services/ both upto an aggregate turnover of Rs. 50 Lacs in any financial year (from 1 April 2019), as under:

CBIC Circular No. 97/16/2019 GST dt. 5 April, 2019

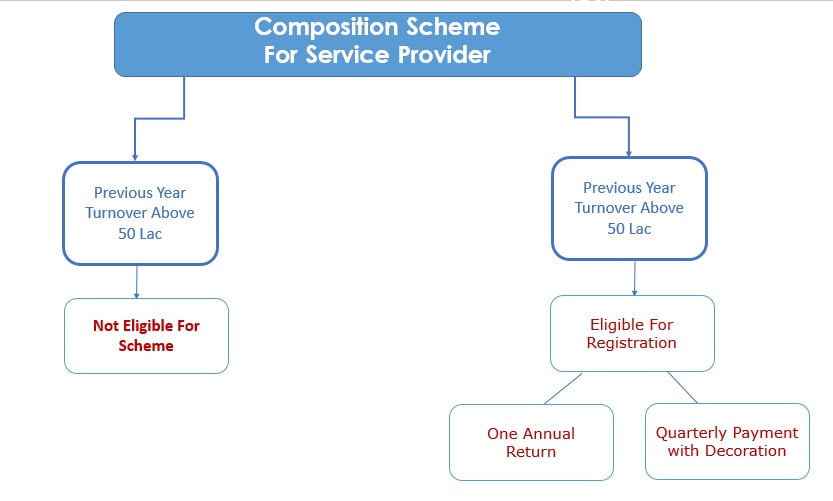

(To give composition scheme for supplier of services with a tax rate of 6% having annual turn over in preceding year upto Rs 50 lakhs.)

(To give composition scheme for supplier of services with a tax rate of 6% having annual turn over in preceding year upto Rs 50 lakhs.)

1. Attention is invited to notification No. 02/2019-Central Tax (Rate) dated 07.03.2019 (hereinafter referred to as “the said notification”) which prescribes rate of central tax of 3% on first supplies of goods or services or both upto an aggregate turnover of fifty lakh rupees made on or after the 1st day of April in any financial year, by a registered person whose aggregate annual turnover in the preceding financial year was fifty lakh rupees or below. The said notification, as amended by notification No. 09/2019-Central Tax (Rate) dated 29.03.2019, provides that Central Goods and Services Tax Rules, 2017 (hereinafter referred to as “the said rules”), as applicable to a person paying tax under section 10 of the Central Goods and Services Tax Act, 2017 (hereinafter referred to as “the said Act”) shall, mutatis mutandis, apply to a person paying tax under the said notification.

2. In order to clarify the issue and to ensure uniformity in the implementation of the provisions of the law across field formations, the Board, in exercise of its powers conferred by section 168 (1) of the said Act, hereby clarifies the issues raised as below:–

2. In order to clarify the issue and to ensure uniformity in the implementation of the provisions of the law across field formations, the Board, in exercise of its powers conferred by section 168 (1) of the said Act, hereby clarifies the issues raised as below:–

(i) a registered person who wants to opt for payment of central tax @ 3% by availing the benefit of the said notification, may do so by filing intimation in the manner specified in sub-rule 3 of rule 3 of the said rules in FORM GST CMP-02 by selecting the category of registered person as “Any other supplier eligible for composition levy” as listed at Sl. No. 5(iii) of the said form, latest by 30th April, 2019. Such person shall also furnish a statement in FORM GST ITC-03 in accordance with the provisions of sub-rule (3) of rule 3 of the said rules.

(ii) any person who applies for registration and who wants to opt for payment of central tax @ 3% by availing the benefit of the said notification, if eligible, may do so by indicating the option at serial no. 5 and 6.1(iii) of FORM GST REG-01 at the time of filing of application for registration.

(iv) the option to pay tax by availing the benefit of the said notification would be effective from the beginning of the financial year or from the date of registration in cases where new registration has been obtained during the financial year.

3. It may be noted that the provisions contained in Chapter II of the said Rules shall mutatis mutandis apply to persons paying tax by availing the benefit of the said notification, except to the extent specified in para 2 above.

0 Comments